How to Choose the Best Life Insurance Policy in the United States

Choosing the right life insurance policy is one of the most important financial decisions you can make. A good life insurance plan provides long-term security for your family, covers outstanding debts, and offers peace of mind in unexpected situations.

This guide explains how to choose the best life insurance in the United States, what factors to consider, and how to avoid common mistakes.

Understand Why You Need Life Insurance

Before selecting a policy, it’s essential to understand your purpose for buying life insurance. In the U.S., people typically purchase life insurance to:

-

Replace lost income for dependents

-

Pay off mortgages, loans, or credit card debt

-

Cover funeral and final expenses

-

Protect children’s future education costs

-

Support a spouse or family member financially

Knowing your main goal helps determine the right type and amount of coverage.

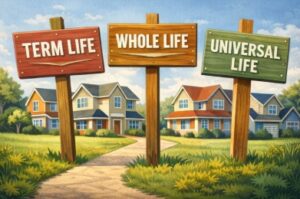

Choose the Right Type of Life Insurance

Term Life Insurance

Term life insurance is the most popular and affordable option in the United States. It provides coverage for a fixed period, usually 10, 20, or 30 years.

Best for:

-

Young families

-

New homeowners

-

Budget-conscious buyers

Whole Life Insurance

Whole life insurance offers lifetime coverage and includes a cash value component that grows over time.

Best for:

-

Long-term financial planning

-

Estate planning

-

People seeking guaranteed benefits

Universal Life Insurance

Universal life insurance combines lifetime coverage with flexible premiums and investment options.

Best for:

-

Those who want adjustable coverage

-

Long-term wealth strategies

-

Higher-income individuals

Determine How Much Life Insurance You Need

A common recommendation in the U.S. is to purchase coverage equal to 10 to 15 times your annual income, but the exact amount depends on:

-

Current income

-

Outstanding debts

-

Number of dependents

-

Future expenses (college, housing, healthcare)

Choosing the right coverage amount ensures your family won’t struggle financially.

Compare Life Insurance Companies Carefully

Not all life insurance companies are the same. When comparing insurers, consider the following:

-

Financial strength ratings (A.M. Best, Moody’s, S&P)

-

Customer satisfaction and reviews

-

Claims payment history

-

Policy flexibility and available riders

Well-known and trusted life insurance providers in the U.S. often offer better long-term reliability.

Review Policy Features and Riders

Life insurance riders can customize your policy. Common riders include:

-

Accidental death benefit

-

Waiver of premium

-

Child rider

-

Living benefits rider

Only add riders that fit your needs, as they can increase premiums.

Understand Premium Costs and Budget

Life insurance premiums depend on several factors, including:

-

Age

-

Health condition

-

Lifestyle habits (smoking, alcohol use)

-

Coverage amount and term length

Buying life insurance earlier in life usually results in lower premiums.

Avoid Common Life Insurance Mistakes

Many Americans make avoidable mistakes when choosing life insurance, such as:

-

Buying too little coverage

-

Choosing price over financial strength

-

Not reviewing policies after life changes

-

Ignoring exclusions and policy terms

Regularly reviewing your policy ensures it remains aligned with your needs.

Work With a Licensed Insurance Agent

A licensed insurance agent can help explain complex terms, compare options, and recommend suitable policies based on your financial goals. Independent agents often provide access to multiple insurers.

Final Thoughts on Choosing Life Insurance in the U.S.

Choosing a good life insurance policy requires planning, research, and understanding your financial responsibilities. With the right approach, life insurance becomes a powerful tool to protect your family’s future.

By selecting the right type of policy, adequate coverage, and a reliable insurance company, you can secure peace of mind and long-term financial stability.

About the Author: Macelo

A professional dedicated to producing informative content for the automotive and insurance sectors, focusing on consumer education and practical analysis of products and services. They develop texts covering topics ranging from vehicle maintenance and use to insurance contracts, coverage comparisons, and risk assessment, always using accessible and up-to-date language.